Millennials and Gen Z are increasingly moving away from traditional homeownership, driven by high housing costs, shifting lifestyle priorities, and evolving financial realities. This article explores the root causes, real-life examples, market implications, and practical advice, helping individuals, investors, and policymakers understand the future of homeownership in America.

Why Many Millennials and Gen Z Are Rejecting Traditional Homeownership

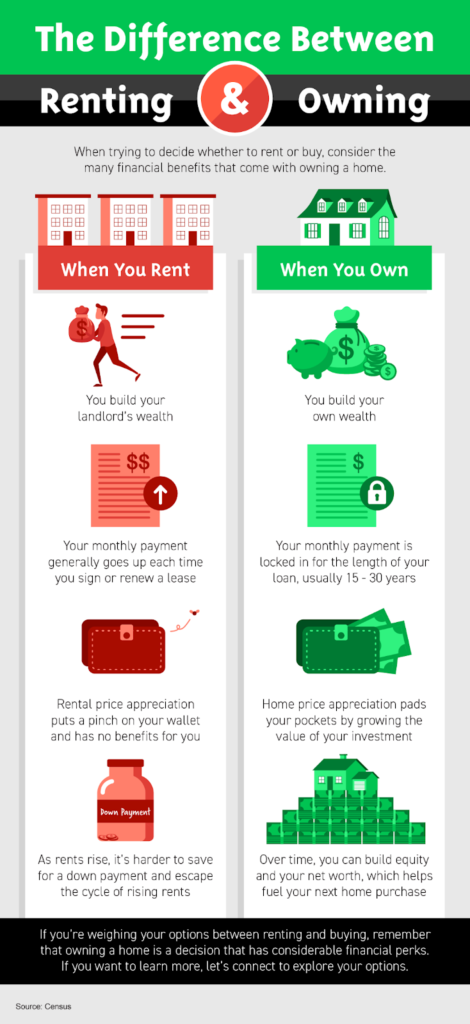

Owning a home has long symbolized stability, wealth accumulation, and achieving the “American Dream.” However, for Millennials (born ~1981–1996) and Generation Z (born ~1997–2012), homeownership is no longer as attainable—or desirable.

Data supports this trend: only 26.1% of adult Gen Zers owned a home in 2024, a figure largely unchanged from previous years (Redfin, 2024). Millennials fared slightly better, with a 54.9% homeownership rate, still stagnant compared to prior years. (Redfin, 2024)

Three main factors are driving this generational shift: affordability constraints, lifestyle and value changes, and structural market shifts.

1. Affordability Constraints

Home prices and mortgage rates have surged while wages and savings haven’t kept pace. According to the Urban Institute, many Millennials are delaying home purchases due to high costs, student debt, and limited affordable inventory (Urban Institute).

For example, young adults face higher down payments, elevated monthly mortgage burdens, and often stagnant incomes, making homeownership challenging compared to previous generations.

2. Lifestyle and Value Shifts

Younger generations are reevaluating the traditional meaning of “homeownership.” Many are delaying marriage, children, or career stability—historically triggers for buying homes—and are prioritizing flexibility, renting, or co-living arrangements.

A Newsweek report notes that many Gen Z and Millennial renters are rejecting starter homes because “it makes no sense anymore” to buy under restrictive market conditions (Newsweek, 2023).

For some, renting offers freedom, mobility, and lifestyle alignment without the burden of debt or long-term commitments.

3. Market Structural Changes

The housing market has fundamentally shifted. Older generations benefited from rising equity, favorable mortgage rates, and abundant entry-level housing. Millennials and Gen Z entered a tighter, costlier market, facing limited supply and higher rates.

For instance, at age 26, only 18% of Gen Z adults owned a home, compared to 25% of Gen Xers at the same age (JB Real Estate Consultants).

Economic disruptions—including the 2008 crisis and the COVID-19 pandemic—have further amplified these challenges.

Real-Life Examples Illustrating the Shift

Example A: Emily, 32, Urban Renter

Emily earns an above-average income in a major metro but finds homeownership prohibitively expensive. Instead, she rents a loft and invests in travel and experiences, prioritizing mobility over a fixed mortgage.

Example B: The Lopez Siblings, 26 & 29

Carlos and Maria both carry student debt and are saving for a down payment. They rent in co-living arrangements while investing in a shared account, choosing flexibility and delayed homeownership.

Example C: First-Time Homebuyers Adapt

A young couple in the Midwest purchases a small, affordable home as an investment property, renting out part of it to offset costs. They demonstrate creative strategies to enter the housing market without traditional starter-home approaches.

What This Trend Means for the Housing Market

Implications for the Market

- Rising Rental Demand: Younger adults delaying homeownership fuel rental market growth.

- Starter-Home Distortion: Entry-level homes may become scarcer or more expensive as demand shifts.

- Wealth Disparities: Delayed or skipped homeownership limits traditional equity-building, potentially widening generational wealth gaps.

- Regional Differences: Expensive or restrictive markets see this trend most sharply, while affordable regions may still attract younger buyers.

Implications for Individuals

- For prospective buyers: Determine whether homeownership aligns with your current financial and lifestyle priorities.

- For investors: Increased rental demand presents opportunities for alternative housing models, including co-buying and shared living.

- For planners: Understand that younger generations may purchase later, requiring flexibility in housing policies and products.

Common Questions Millennials and Gen Z Are Asking

Q1: Why are younger generations less likely to buy homes?

High housing costs, delayed milestones, student debt, and tighter financing all contribute to lower homeownership rates.

Q2: Can wealth still be built without owning a home?

Yes—strategies include investing in stocks, retirement accounts, and other assets, or purchasing property in more affordable markets.

Q3: Is renting always worse than buying?

Not necessarily. Renting can provide flexibility and avoid the financial strain of purchasing a home prematurely.

Q4: How does debt affect homeownership?

Student loans and other debts reduce savings for down payments, affect credit profiles, and limit mortgage eligibility.

Q5: Are Millennials and Gen Z giving up on homeownership entirely?

Many are delaying or rethinking timing but still view homeownership as a long-term goal.

Q6: Which markets allow younger buyers to purchase homes?

Affordable regions like parts of the Midwest and Sun Belt cities, or areas with emerging job markets, provide opportunities.

Q7: How long will younger generations wait to buy?

The median age of first-time buyers in the U.S. is now 38, up from 35 the year prior. (Newsweek)

Q8: What should buyers prioritize today?

Affordability, realistic budgeting, property quality, long-term goals, and flexibility in renting or co-owning are key.

Q9: What alternatives exist to traditional homeownership?

- Long-term renting with concurrent investments

- Co-buying with friends/family

- Purchasing smaller or less expensive properties

- Investing in shared housing arrangements

Q10: How will this trend influence policy and the market?

Housing affordability, first-time buyer programs, zoning reforms, and wealth-building strategies will need adaptation to meet delayed or changing homeownership patterns.

Practical Advice for Younger Adults

- Recognize homeownership isn’t automatic: Consider it one of many housing paths.

- Prioritize affordability: Avoid stretching finances too thin.

- Align with life stage and goals: Timing matters more than “keeping up.”

- Explore alternative paths: Renting or co-buying can be strategic choices.

- Stay informed on local markets: Track supply, mortgage rates, and affordability.