Home prices across the U.S. are behaving in unexpected ways—rising in some regions, stalling or slipping in others, and confusing buyers nationwide. This is not a housing crash or a new boom. Instead, it’s a market recalibration driven by affordability limits, regional divergence, supply constraints, and shifting buyer psychology. Buyers shouldn’t panic—but they do need to adjust expectations and strategy.

Introduction: Why the Housing Market Feels Unsettling Right Now

If you’re a homebuyer today, chances are you feel conflicted. One headline claims home prices are still climbing. Another warns that buyers are pulling back. Friends tell you to “wait for the crash,” while real estate agents insist now is the moment to act.

This emotional whiplash isn’t accidental. The U.S. housing market is in a transition phase, and transitions are always uncomfortable. Prices aren’t behaving the way people expect. They’re not falling sharply, yet affordability feels worse than ever. Homes aren’t flying off the market, yet sellers aren’t panicking either.

That contradiction is what makes this moment feel strange.

To make smart decisions, buyers must understand why prices look stable on the surface, what’s quietly changing underneath, and whether concern—not fear—is the appropriate response.

What Exactly Is “Strange” About Home Prices Today?

In a normal housing cycle, prices either rise quickly or fall decisively. Today’s market does neither.

Instead, we’re seeing:

- Flat or modest price growth nationally

- Sharp differences between cities and neighborhoods

- More price cuts, but fewer dramatic drops

- Rising negotiation power without falling list prices

In other words, prices look firm—but behavior tells a different story.

Homes sit longer on the market. Buyers hesitate. Sellers test pricing, then adjust. Transactions still happen, but without the urgency that defined the past few years.

This disconnect between price data and lived experience is what’s confusing buyers most.

Is This the Beginning of a Housing Crash?

This is the question dominating search engines:

“Are home prices about to crash?”

The evidence strongly suggests no.

A housing crash requires forced selling. Today, forced selling is rare. Most homeowners:

- Locked in low fixed-rate mortgages

- Built substantial equity

- Face no urgency to sell

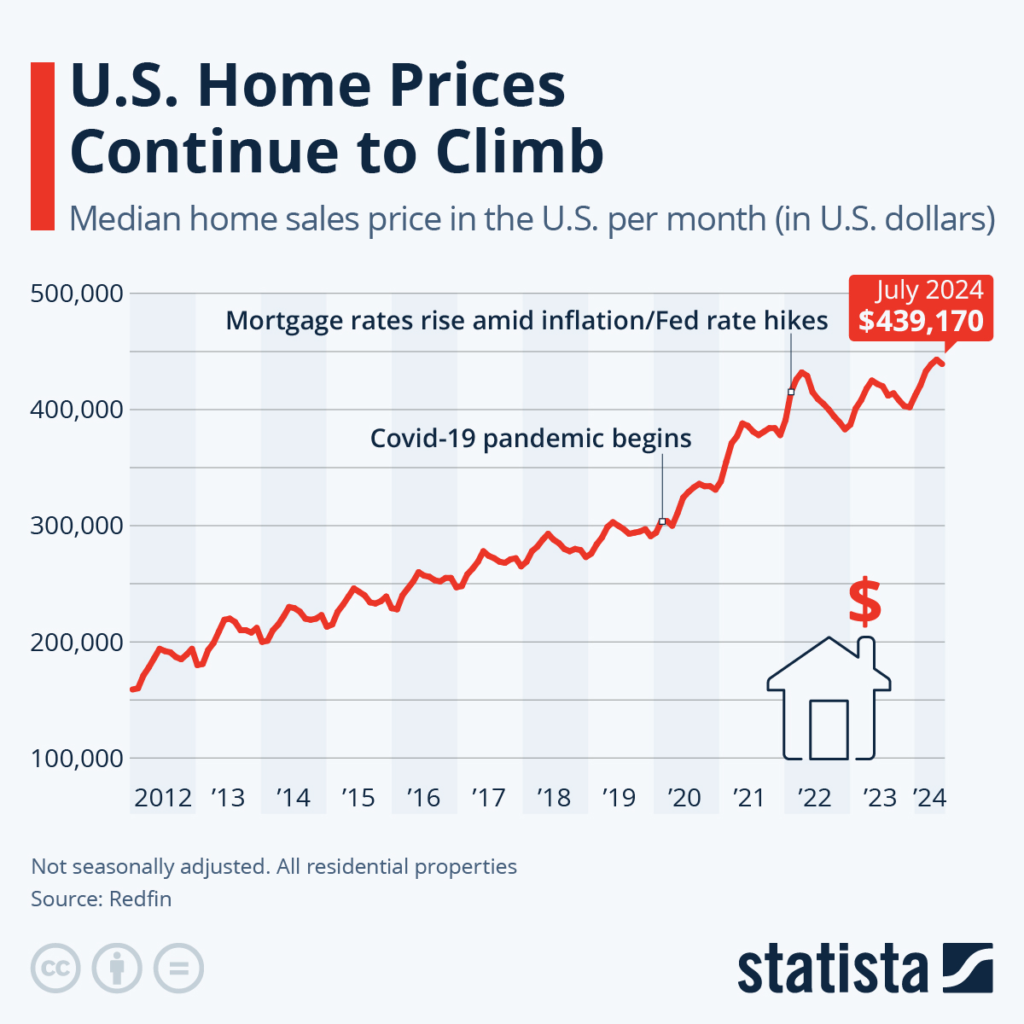

According to housing finance data tracked by Freddie Mac, the vast majority of mortgages are fixed-rate, and delinquency rates remain historically low.

Without distress, prices don’t collapse—they stagnate, drift, or adjust slowly.

This is exactly what we’re seeing now.

Why Mortgage Rates Didn’t Trigger a Price Collapse

Many buyers assumed that once mortgage rates rose sharply, prices would follow. That assumption ignored a crucial reality: supply never recovered.

The U.S. entered this decade with a structural housing shortage caused by:

- Years of underbuilding after 2008

- Zoning restrictions

- Labor and material constraints

When rates rose, demand cooled—but supply stayed tight. That imbalance prevented a sudden price drop.

Instead, prices paused.

The result is a market where affordability worsened without prices falling—a frustrating but economically logical outcome.

Why Prices Are Still Rising in Some Cities

Buyers often ask, “Why are prices still going up where I live?”

Prices tend to remain resilient in areas with:

- Strong job growth

- High household incomes

- Limited land availability

In these regions, buyers may complain about rates—but they can still qualify. Demand softens, but doesn’t disappear.

This is why national averages are misleading. There is no single U.S. housing market—only local markets reacting differently to the same pressures.

Why Prices Are Quietly Falling in Other Markets

At the same time, certain markets are cooling faster—especially those that surged during the pandemic.

Common traits include:

- Heavy investor activity in prior years

- Rapid population inflows that have since normalized

- Affordability stretched beyond local incomes

In these areas, sellers are more likely to cut prices or offer incentives. The declines are subtle, not dramatic, which is why many buyers miss them.

Opportunity exists—but only for those paying attention.

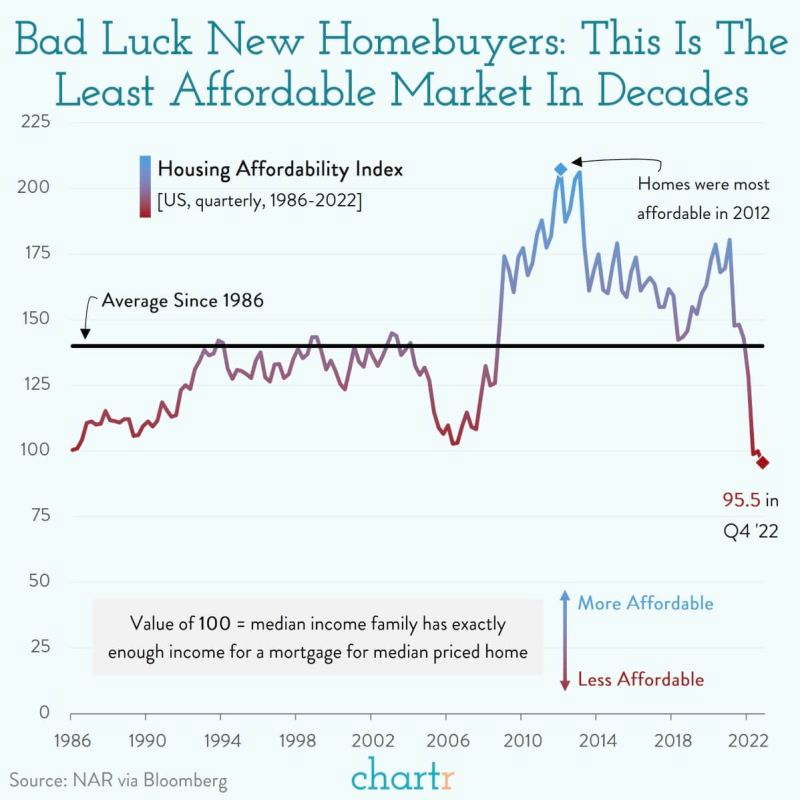

The Affordability Ceiling Buyers Keep Hitting

One of the most important concepts shaping today’s housing market is the affordability ceiling.

There is a limit to what buyers can pay monthly, regardless of how much they want a home. Higher rates brought many buyers to that limit faster than expected.

As a result:

- Buyers refuse to bid beyond comfort levels

- Demand weakens before prices collapse

- Sellers must adjust expectations slowly

This creates sideways price movement instead of sharp declines.

Why Buyers Feel Worse Even When Prices Don’t Fall

Many buyers feel more anxious today than during the peak frenzy—and that seems counterintuitive.

The reason is simple: monthly payments matter more than prices.

A home priced the same as two years ago may now cost hundreds—or thousands—more per month. That financial pressure creates emotional stress, even if prices appear stable.

This gap between perception and reality fuels fear-driven headlines—but not necessarily fear-driven outcomes.

Are Sellers Finally Losing the Upper Hand?

For the first time in years, sellers no longer control every aspect of the transaction.

Today, sellers are increasingly:

- Accepting inspection negotiations

- Offering credits and rate buydowns

- Adjusting prices earlier to avoid stagnation

While sellers still benefit from limited supply, the balance of power is shifting toward neutrality.

That shift is subtle—but significant.

What First-Time Buyers Are Actually Experiencing

First-time buyers are often the most anxious group, having watched prices surge beyond reach only to face higher rates later.

Yet many are now:

- Buying without bidding wars

- Securing seller concessions

- Taking time to evaluate options

The market no longer rewards speed. It rewards preparation, patience, and financial discipline.

Should Buyers Wait for Prices to Drop?

This is the most difficult question—and the most personal.

Waiting can make sense if:

- Your finances are stretched

- Inventory is rising rapidly in your area

- You expect life changes soon

But waiting also carries risks:

- Rents may continue rising

- Competition could return if rates fall

- Desired homes may disappear

Successful buyers focus less on predicting prices and more on long-term affordability and stability.

Investors Are Pulling Back—And That’s Healthy

Investor demand played a major role in pushing prices higher during the boom years. That activity has cooled.

Higher financing costs and slower appreciation mean speculation no longer works. What remains are disciplined investors focused on fundamentals.

This reduces artificial demand and helps stabilize prices for primary buyers.

New Construction’s Quiet Role in Stabilizing Prices

Homebuilders have adapted faster than many realize.

Instead of overbuilding, many are:

- Reducing home sizes

- Offering aggressive incentives

- Targeting entry-level buyers

This controlled supply expansion prevents sharp price drops while easing long-term shortages.

What the Data Suggests Comes Next

Aggregated housing forecasts from platforms like Zillow suggest national home prices will remain mostly flat, with significant local variation.

Meanwhile, guidance from the Federal Reserve indicates policymakers are watching housing affordability closely, recognizing its influence on inflation and consumer stability.

The consensus outlook: volatility without collapse.

Practical Guidance for Buyers Feeling Uneasy

Instead of worrying about headlines, buyers should focus on controllable factors:

Smart buyer priorities include:

- Monthly payment comfort

- Local market data, not national noise

- Negotiation leverage

- Long-term ownership plans

Confidence comes from clarity—not prediction.

Frequently Asked Questions (FAQ)

1. Are home prices about to crash?

No. Current conditions point to stabilization and localized adjustments, not a nationwide crash.

2. Why are home prices still high despite high mortgage rates?

Because housing supply remains constrained and most owners are not forced to sell.

3. Is it risky to buy a home right now?

Risk depends on personal finances and time horizon, not headlines.

4. Will prices drop if mortgage rates fall?

Lower rates could actually increase demand and support prices.

5. Are sellers negotiating more now?

Yes. Negotiation power has improved significantly for buyers.

6. Should first-time buyers wait?

Only if waiting improves affordability or life flexibility.

7. Are price cuts becoming common?

Yes, especially in markets that overheated earlier.

8. Is renting safer than buying right now?

Renting offers flexibility, but long-term costs still matter.

9. What’s the biggest mistake buyers are making?

Trying to perfectly time the market instead of planning sustainably.

10. When will housing feel normal again?

Normal is evolving—but balance is gradually returning.

Final Thoughts: Caution Is Healthy—Fear Is Not

Home prices are doing something unusual because the market itself is changing. This isn’t a warning sign of collapse—it’s evidence of recalibration.

Buyers who understand this moment gain leverage and confidence. Those who react emotionally risk missing opportunities that appear quietly during uncertainty.

The housing market isn’t breaking. It’s adapting—and informed buyers can adapt with it.