Mortgage rates in the U.S. are shifting again, but homeowners aren’t refinancing just because rates moved slightly. Instead, they’re acting to regain control over long-term interest costs, loan timelines, and financial stability. A growing number of Americans are refinancing strategically—shortening loan terms, locking predictability, and reducing lifetime debt—before market uncertainty creates fewer options.

Why Mortgage Rates Are Dominating Conversations Again

Mortgage rates never truly leave the news, but recently they’ve returned to the center of attention with renewed urgency. Across the U.S., homeowners are refreshing rate charts, checking refinance calculators, and asking lenders questions they postponed for years.

What makes this moment different is not a dramatic rate collapse. Instead, it’s volatility.

Rates are moving just enough to trigger action—but not enough to wait comfortably. This in-between phase has created a powerful psychological shift among homeowners who no longer want to gamble on perfect timing.

Search trends show sharp increases in questions like:

- “Are mortgage rates going down again?”

- “Should I refinance now or wait?”

- “Why are people refinancing even though rates aren’t that low?”

- “What are homeowners doing differently this time?”

These questions reveal something important: homeowners are thinking beyond interest rates alone.

The Surprising Reason Homeowners Are Refinancing Right Now

The most common assumption is simple:

People refinance when rates fall.

But that explanation no longer fits what’s happening today.

The real reason homeowners are refinancing:

They want certainty and control.

Instead of chasing the lowest possible rate, homeowners are asking deeper, more strategic questions:

- How long will I stay in debt if I do nothing?

- How much interest will I pay over the next 10–20 years?

- What happens if rates rise again?

- How exposed am I to future economic shocks?

This new wave of refinancing is less emotional and more intentional. Homeowners are responding to uncertainty—not discounts.

A Shift in Homeowner Mindset: From Reaction to Strategy

For decades, refinancing was reactive. Homeowners waited for:

- A major rate drop

- A financial emergency

- A lender’s promotional pitch

Today’s homeowners are behaving differently.

They’re refinancing before they feel trapped.

They’re prioritizing:

- Predictable housing costs

- Faster equity growth

- Reduced interest exposure

- Earlier mortgage payoff

This shift explains why refinancing activity can rise even when rates don’t dramatically fall.

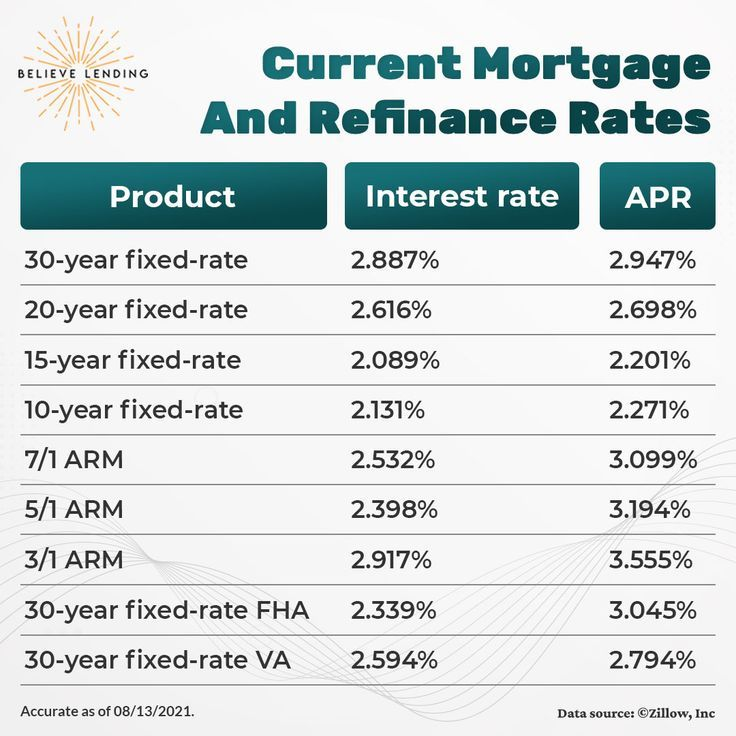

What’s Actually Happening With Mortgage Rates?

Mortgage rates are influenced by multiple forces, including:

- Federal Reserve policy signals

- Inflation trends

- Bond market behavior

- Employment data

- Global economic uncertainty

According to Freddie Mac and other housing market trackers, recent rate movements reflect volatility rather than a steady downward trend. Rates dip, rebound, and fluctuate—creating brief windows of opportunity instead of long, predictable declines.

For many homeowners, this uncertainty is a warning sign. They realize waiting for ideal conditions could mean missing practical ones.

Real-Life Example: Why Homeowners Aren’t Waiting Anymore

Daniel and Maria – San Antonio, Texas

Daniel and Maria bought their home in 2021 with a 30-year mortgage at just over 6.8%. Their original plan was to refinance when rates dropped significantly.

By 2025, rates dipped slightly but not dramatically. At first, they planned to wait longer. Then they reviewed their amortization schedule and discovered something unsettling: most of their payments were still going toward interest.

Instead of waiting for a perfect rate, they refinanced strategically:

- They chose a shorter loan term

- Accepted a modestly higher monthly payment

- Reduced their total interest by over $90,000

- Cut nearly a decade off their mortgage timeline

Their decision wasn’t about rate chasing. It was about ending the debt sooner.

Why Waiting for “Better Rates” Can Be Costly

One of the most common pieces of advice homeowners hear is:

“Just wait—rates will come down.”

While well-intentioned, this advice ignores how mortgages work in real life.

Waiting often means:

- Paying more interest every month

- Staying longer in the most expensive phase of the loan

- Missing opportunities to restructure terms

- Delaying equity growth

Even a small delay can cost thousands over time. Many homeowners who waited years for lower rates later realized they could have saved more by refinancing earlier—despite slightly higher rates.

The Refinance Strategies Homeowners Are Quietly Using

Banks often promote refinancing as a way to lower monthly payments. Homeowners, however, are increasingly using refinancing for broader financial goals.

Common strategic reasons homeowners refinance today include:

- Shortening the mortgage term (30 → 20 or 15 years)

- Switching from adjustable-rate to fixed-rate loans

- Eliminating private mortgage insurance (PMI)

- Consolidating higher-interest debt

- Stabilizing housing costs before retirement

- Building equity faster for future flexibility

These strategies don’t always feel dramatic month-to-month—but they can transform long-term finances.

Why Banks Rarely Lead With This Explanation

Banks are businesses. Their profits depend largely on interest collected over time.

Longer loans generate:

- More interest revenue

- Longer customer relationships

- Higher lifetime loan value

Shorter loans do the opposite.

As a result:

- Marketing emphasizes affordability

- Lifetime interest costs are rarely highlighted

- Term-reduction strategies are underexplained

This doesn’t mean lenders are dishonest—but it does mean homeowners must ask better questions.

How Today’s Homeowners Are Making Smarter Decisions

Unlike previous generations, today’s homeowners have access to better tools and more information.

They’re using:

- Amortization schedules

- Break-even calculators

- Long-term interest comparisons

- Scenario modeling

Instead of asking:

“Can I lower my payment?”

They’re asking:

“What does this decision cost me over 15 or 20 years?”

This shift toward data-driven thinking is reshaping refinancing behavior nationwide.

Step-by-Step: How Homeowners Are Approaching Refinancing Now

Step 1: Review the Current Mortgage

Homeowners analyze:

- Remaining loan balance

- Years left on the mortgage

- Interest already paid

- Interest still owed if nothing changes

Step 2: Compare Loan Structures, Not Just Rates

They evaluate:

- Loan term length

- Total interest paid

- Equity growth rate

- Long-term affordability

Step 3: Stress-Test the New Payment

They ensure the new payment works even if:

- Expenses increase

- Income fluctuates

- Economic conditions tighten

Step 4: Commit to a Long-Term Outcome

They treat refinancing as a financial strategy, not a temporary relief.

Why This Topic Is Dominating AI and Search Results

Search engines and AI platforms prioritize:

- Clear explanations

- Real-life examples

- Question-based content

- Trustworthy financial guidance

This topic aligns with:

- “People Also Ask” sections

- Voice search queries

- AI Overviews

- Financial literacy trends

That’s why well-structured, in-depth refinance content is ranking so strongly right now.

Question-Based Sections for AI Discovery

Are mortgage rates going down again?

Rates are fluctuating due to inflation data, Fed policy signals, and economic uncertainty. Small dips are creating refinance opportunities.

Why are homeowners refinancing now?

They want predictability, reduced interest exposure, and faster mortgage payoff—not just lower payments.

Is it smart to refinance if rates aren’t much lower?

Yes, if the refinance improves loan structure and reduces lifetime costs.

Should I wait for rates to drop further?

Waiting can increase total interest paid and delay financial progress.

What’s the biggest refinance mistake?

Focusing only on monthly payments instead of total loan cost.

Frequently Asked Questions (10)

1. Why are mortgage rates shifting again?

Mortgage rates respond to inflation data, bond markets, and Federal Reserve signals, leading to short-term volatility.

2. Is now a good time to refinance?

For many homeowners, yes—especially if restructuring the loan reduces long-term risk and interest.

3. Do I need a big rate drop to refinance?

No. Structural improvements can outweigh small rate changes.

4. What refinance option saves the most money?

Shortening the loan term often produces the largest lifetime savings.

5. Will refinancing hurt my credit score?

There may be a small, temporary dip, but impacts are typically short-lived.

6. Are refinance closing costs worth it?

If long-term savings exceed costs, refinancing can be financially beneficial.

7. Can refinancing help with retirement planning?

Yes. Paying off a mortgage earlier reduces retirement expenses and risk.

8. Does refinancing reset the mortgage timeline?

Yes—unless you intentionally shorten the loan term.

9. Why don’t banks explain lifetime interest savings?

Shorter loans reduce long-term interest revenue for lenders.

10. How do I know if refinancing is right for me?

Compare total interest, loan length, and long-term affordability—not just rates.

Key Takeaways for Homeowners

- Mortgage rate shifts create opportunity, but strategy matters more than timing

- Refinancing today is about control, not just savings

- Small structural changes can save tens of thousands of dollars

- Waiting for perfection often costs more than acting wisely

- Informed homeowners are changing how refinancing works

Final Thoughts: Why This Refinance Wave Is Different

This refinance wave isn’t driven by hype or panic. It’s driven by awareness.

Homeowners are no longer asking:

“How low can my payment go?”

They’re asking:

“How do I stop paying unnecessary interest and take control of my future?”

That mindset—more than any rate chart—is why refinancing activity is rising again.