Millions of Americans are on the brink of a major financial crisis as elevated interest rates collide with record household debt and shrinking savings. This article breaks down why borrowing costs continue rising, who is most vulnerable, how mortgages, credit cards, auto loans, and student loans will be affected, and practical steps to protect your finances before the “interest rate shock” hits full force.

Introduction

For more than a decade, Americans enjoyed the benefits of historically low interest rates. Borrowing was cheap, mortgages were affordable, and credit card interest—while still high—wasn’t nearly as punishing as it is today. But the financial landscape has shifted dramatically. With the Federal Reserve holding rates at their highest levels in 22 years and household debt reaching unprecedented highs, millions of Americans are walking straight into an Interest Rate Horror they never saw coming.

This crisis is unlike anything the country has faced in modern economic history. It isn’t a sudden collapse like 2008. Instead, it is a slow, grinding, painful squeeze that is placing enormous pressure on middle-class families, young professionals, homeowners, renters, small business owners, and anyone carrying revolving debt.

According to the New York Federal Reserve, U.S. household debt has now surpassed $17.5 trillion, while credit card delinquencies have risen at the fastest pace since the Great Recession. Yet many Americans still underestimate how deeply interest rates will affect their daily lives in the months ahead.

This article dives into the causes behind the interest rate crisis, who will be hit the hardest, what the next 12–24 months may look like, and the practical steps you must take to protect your financial future.

Why Millions Are Facing a Coming Interest Rate Crisis

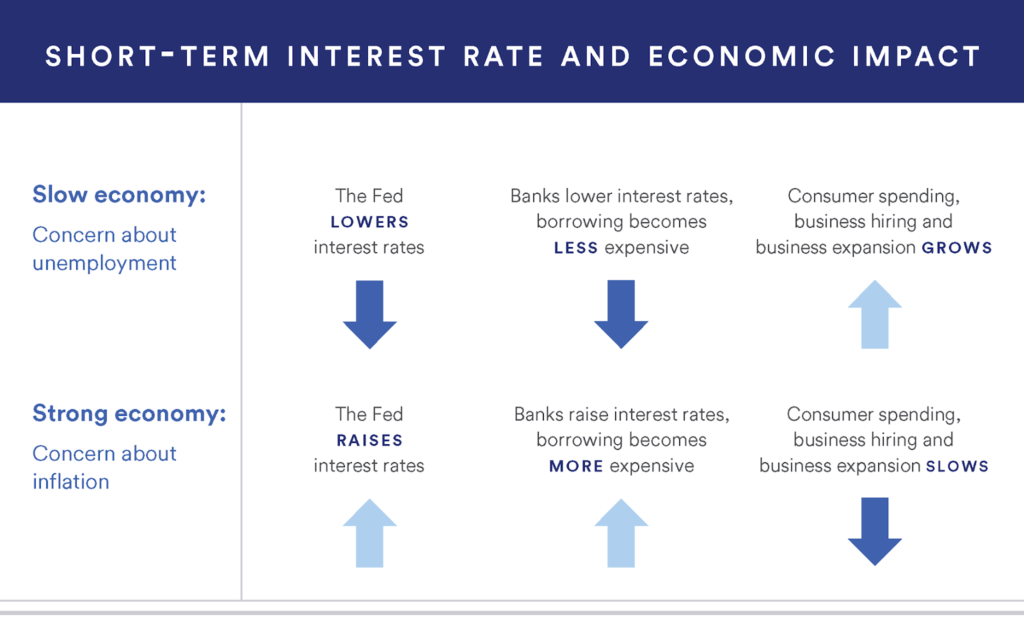

Interest rates may seem like something that only banks and economists worry about, but they influence nearly every major financial decision you make: buying a home, purchasing a car, using a credit card, paying off student loans, or even starting a business.

Today’s interest rate environment is the result of three powerful forces converging at the same time:

1. The Federal Reserve Is Keeping Rates “Higher for Longer”

Inflation may have cooled from its 40-year highs, but it is still above the Fed’s preferred 2% target. That means the Federal Reserve is reluctant to cut rates aggressively. Even modest rate cuts will not bring borrowing costs anywhere close to pre-2020 levels.

Many Americans assumed inflation falling meant interest rates would immediately drop — but the Fed has repeatedly emphasized caution. As a result, even “small” cuts will not relieve the pressure borrowers are facing.

2. Debt Levels Are at Record Highs

Americans owe more today than ever before:

- Credit card debt: $1.08 trillion

- Auto loan debt: $1.62 trillion

- Mortgage debt: $12.5 trillion

- Student loan debt: $1.77 trillion

During the low-rate years, households became more comfortable taking on debt. Now those debts are becoming dramatically more expensive to carry — especially for people with variable-rate loans or credit cards.

3. Pandemic Savings Have Vanished

During COVID, American households accumulated more than $2.1 trillion in excess savings due to stimulus programs and reduced spending. Today, those savings are nearly gone.

Studies show 61% of Americans now live paycheck to paycheck, and nearly half cannot handle a $1,000 emergency without using credit.

That means any increase in borrowing costs can quickly turn into a crisis.

Who Is Most at Risk as Interest Rates Remain High?

While rising rates affect everyone, certain groups are far more vulnerable. You are at heightened risk if:

• You carry a credit card balance

With APRs reaching 22–28%, your debt could double faster than expected.

• You have an adjustable-rate mortgage (ARM)

Millions of ARM loans will reset within the next few years, causing monthly payments to spike.

• You plan to buy a home or refinance soon

Mortgage affordability is at its lowest in more than 40 years.

• You rely on a small business credit line

Higher rates are crushing small businesses across the country.

• You have private or variable-rate student loans

Some borrowers have seen interest jump from 3% to over 10%.

In other words… if you owe money, you’re at risk.

How High Interest Rates Are Reshaping the American Economy

This isn’t just a financial issue — it’s a lifestyle shift. Rising borrowing costs are changing how Americans spend, save, and think about their futures.

Let’s break down the areas where the pain is intensifying.

1. Mortgage Shock: Homeowners Are Facing Severe Payment Increases

Millions of homeowners who took out mortgages between 2017 and 2021 are about to be hit with resets, refinances, and significantly higher rates.

Real-Life Case Study:

Michael, a homeowner in Texas, took out a 5/1 ARM mortgage in 2019 with an introductory rate of 2.9%. When his fixed period ended this year, his rate jumped to 7.2%. His monthly payment increased by $740 — instantly.

Michael shared:

“We budgeted for everything except this. We never thought the rate could jump that much.”

Multiply this by millions of households and the pressure becomes clear.

Even renters are affected — landlords facing higher financing costs are raising rents to compensate.

2. Credit Card Interest: A Growing Disaster

Credit card APRs have reached their highest levels in modern American history.

- Average APR (2020): 16%

- Average APR (today): 22–28%

A typical $7,000 credit card balance could take decades to pay off when only minimum payments are made.

Real-Life Story:

Sarah, a 29-year-old teacher in Ohio, watched her APR jump from 18.99% to 27.99%. Her minimum payment increased from $140 to $210 — and most of that now goes toward interest.

Her words:

“I’m paying more in interest than I am in my actual debt.”

This is becoming increasingly common across the country.

3. Auto Loan Payments Are Becoming Unaffordable

Car loans have also been hit dramatically:

- New car APR: 7.2–10%

- Used car APR: 11–17%

The average new car payment is now over $750 per month — the highest in history.

Many Americans are “auto debt trapped,” unable to refinance without paying more, and unable to sell because their loans exceed their vehicle’s value.

4. Student Loan Payments Are Back — and More Burdensome

When federal student loan payments resumed after a three-year pause, many borrowers were already stretched thin.

Private student loan borrowers with variable rates were hit even harder, with interest jumping from 3–5% to 10–12%.

Rising student loan payments are driving many households into deeper credit card debt, creating a dangerous cycle.

5. Small Business Owners Are in Crisis Mode

Small businesses rely on credit lines to maintain cash flow. Today, those credit lines come with interest rates of:

- 11%–19% on average

- Higher for businesses with weaker credit

Business Owner Example:

A bakery owner in California saw her credit line renewal jump from 7.25% to 14.9%.

She said:

“The interest alone equals two months of payroll.”

When small businesses struggle, local economies do too. Prices go up. Hiring slows. And communities suffer.

The Questions Americans Are Asking Right Now (SEO Search Clusters)

These are the urgent questions people are typing into Google daily — and the answers matter.

Why are interest rates still so high?

Because inflation remains above target, and the Fed is prioritizing economic stability over affordability.

Will interest rates go down in 2025?

Possibly, but not significantly. Borrowing costs will likely remain high for years.

Are we heading toward a credit card crisis?

Yes. Delinquencies are rising at their fastest pace since the 2008 recession.

Who will be hit hardest?

Young professionals, middle-class families, and anyone with variable-rate or revolving debt.

How to Protect Yourself From the Interest Rate Horror

Here are actionable steps you can take immediately to reduce your financial risk:

1. Refinance High-Interest Debt

Even a small APR reduction can save thousands per year.

2. Shift balances to 0% intro APR cards

Some offer 12–21 months of interest-free repayment.

3. Avoid new loans unless absolutely necessary

Today’s rates make borrowing extremely expensive.

4. Build a 90-day emergency fund

This buffer can prevent financial collapse.

5. Consolidate debt through a fixed-rate loan

Predictable payments help stabilize your budget.

6. Cut subscriptions and recurring expenses

These drain more money than most people realize.

7. Negotiate debt terms with lenders

Most lenders now offer hardship programs.

8. Increase income through side gigs

Every extra dollar helps offset rising costs.

9. Check your credit score weekly

Lenders are tightening approval requirements.

10. Consult a financial advisor

Professional guidance can prevent long-term damage.

10 Frequently Asked Questions (FAQs)

1. Will the interest rate crisis get worse in 2025?

Yes. Millions of mortgages and loans will reset at higher rates, worsening affordability.

2. Is high inflation still a problem?

Inflation is lower, but still above the Federal Reserve’s 2% target — which keeps rates elevated.

3. Should I buy a home now or wait?

Many experts recommend waiting unless you find an undervalued property or have strong financial stability.

4. Are credit card delinquencies rising?

Yes. They’re climbing at their fastest pace since the Great Recession.

5. Will mortgage rates return to 3%?

No. That era is gone for the foreseeable future.

6. Are auto loans becoming unaffordable?

Yes. Payments now resemble rent-sized monthly obligations.

7. Will student loan interest rates drop?

Not significantly for private borrowers.

8. Should I consolidate debt right now?

Yes — consolidating earlier protects you from further rate hikes.

9. How do higher interest rates impact my credit score?

Missed or late payments caused by higher minimums can lower your score.

10. What’s the biggest financial risk this year?

Carrying high-interest or variable-rate debt during a prolonged high-rate environment.

Final Takeaway: Are You Prepared?

The interest rate crisis is not a theoretical threat — it’s already happening. Millions of Americans will face rising payments, tightening budgets, shrinking purchasing power, and increased financial stress.

But preparation can turn fear into control.

By taking steps now — reducing debt, consolidating loans, increasing income, and carefully planning major expenses — you can survive and even thrive in this high-rate era.

The interest rate horror is coming.

Preparation is optional — consequences are not.