Most Americans don’t realize how deeply the Federal Reserve influences housing prices. Through mortgage-rate manipulation, balance-sheet strategies, and indirect market pressure, the Fed quietly shapes affordability, supply, and demand. This article uncovers the subtle mechanisms behind the Fed’s hidden involvement in the housing market and reveals how these actions impact borrowers, homeowners, and renters today.

Introduction: Is the Federal Reserve Quietly Managing the Housing Market?

For decades, Americans have watched home prices climb faster than wages, leaving millions wondering why the dream of homeownership feels increasingly out of reach. While many factors contribute to the volatility of the housing market—supply shortages, demographic shifts, Wall Street investors—another powerful force operates behind the scenes: the Federal Reserve.

Most people believe the Fed only sets interest rates. But its influence over the housing market goes much deeper. Through subtle policy signals, strategic balance-sheet moves, and indirect market manipulation, the Fed has the power to cool down, heat up, or stabilize the nation’s housing prices without ever admitting to doing so.

This isn’t conspiracy. It’s economics—mixed with quiet policy engineering that affects every American who pays rent, owns a home, or hopes to buy one.

Why Would the Fed Want to Control Housing Prices?

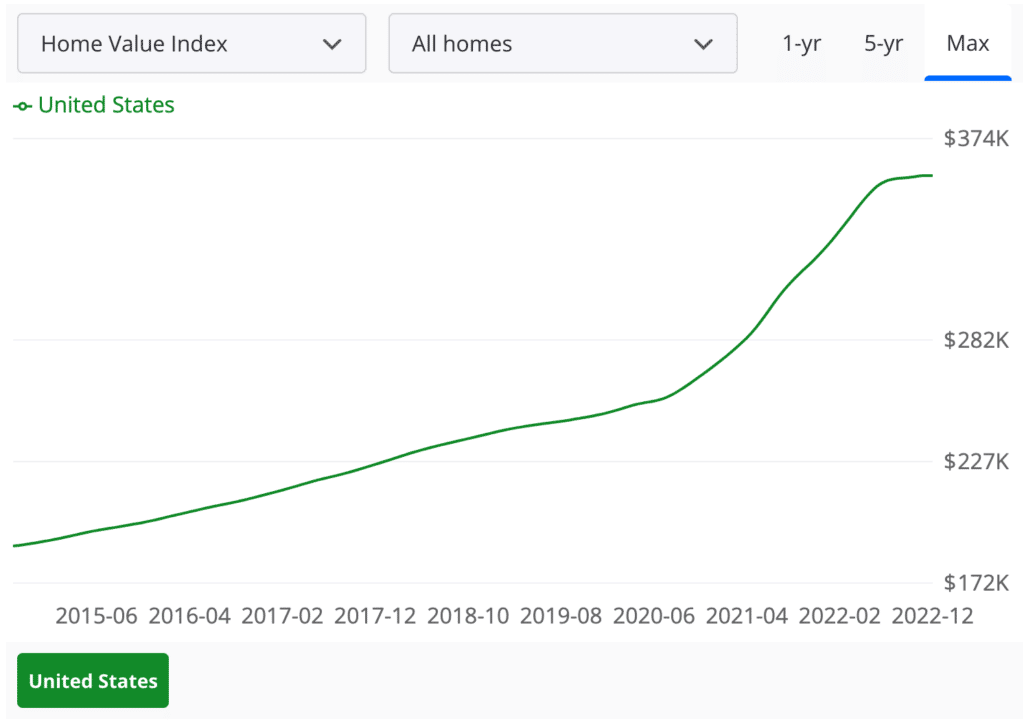

Housing is the largest component of household wealth in the United States. According to Federal Reserve data (2024), Americans hold nearly $49 trillion in residential real estate wealth. When home prices crash, consumer confidence collapses, banks lose liquidity, and the economy plunges into recession.

So the Fed has strong reasons to keep the housing market “stable”:

- A stable housing market supports economic growth

- Rising home equity creates financial confidence

- Crashes threaten banks, jobs, and GDP

- Housing inflation strongly influences the Consumer Price Index (CPI)

But stability is subjective. What feels “stable” to policymakers often feels expensive and unattainable to regular Americans.

What Signs Show the Fed Is Quietly Targeting Housing Prices?

The Federal Reserve will never publicly announce that it’s trying to control home prices. But its patterns reveal a consistent strategy.

Here are the clearest indicators:

1. Massive Purchases of Mortgage-Backed Securities (MBS)

After 2008, and again during the pandemic, the Fed bought more than $2.7 trillion in MBS. These purchases kept mortgage rates artificially low—fueling demand and lifting home prices.

It was an intentional move to stimulate the housing market.

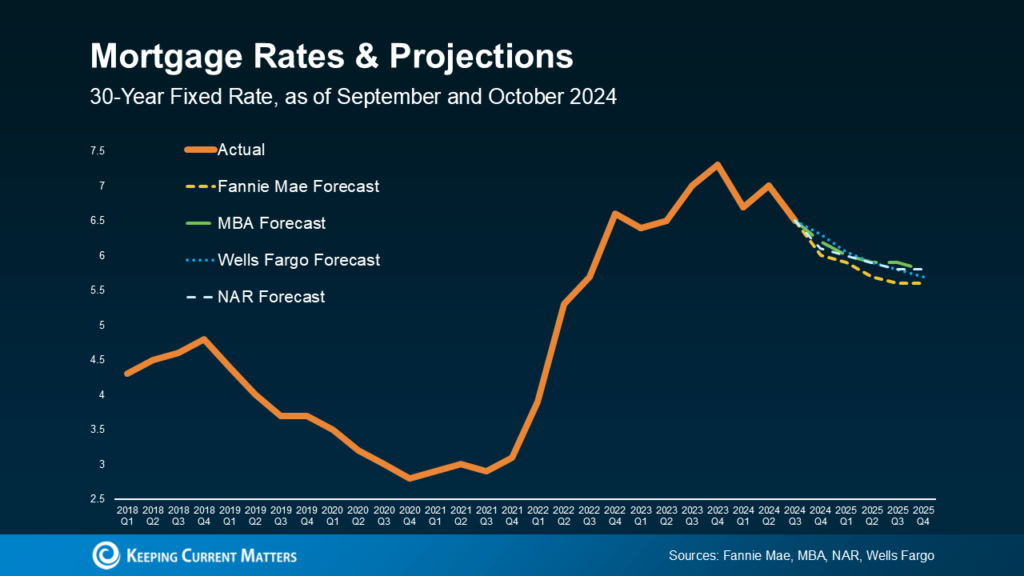

2. Strategic, Aggressive Interest Rate Hikes (2022–2023)

When inflation surged, the Fed raised rates at the fastest pace in 40 years. Mortgage rates jumped above 7%, reducing demand.

But the Fed repeatedly stressed that a “housing crash” must be avoided.

In other words:

Cool the market—but not enough to collapse it.

3. Gradual, Controlled Balance Sheet Reduction

Instead of rapidly offloading its massive MBS holdings, the Fed has slowed the pace, clearly signaling that it does not want mortgage rates to spike too high too fast.

4. Repeated Public Commentary on Housing Affordability

Although the Fed claims it does not target specific market sectors, its officials routinely mention:

- Housing inflation

- Unsustainable appreciation

- Affordability concerns

- Shelter costs in CPI

This unusual attention indicates that housing is a priority—even if not officially stated.

How the Fed Influences Housing Prices (Explained Simply)

Even though the Fed doesn’t directly set mortgage rates or home prices, its actions indirectly shape both. Here’s how the system works in the real world.

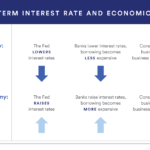

1. Mortgage Rates React to Fed Policy

Mortgage rates rise or fall based on:

- Rate hikes

- Forward guidance

- Treasury yields

- Inflation expectations

A single speech by the Fed chair can move mortgage rates within minutes.

Example:

In late 2023, Jerome Powell’s warning about “persistent inflationary pressures” caused mortgage rates to rise overnight—even though the Fed had not changed rates.

2. Mortgage-Backed Securities Purchases Manipulate Lending Costs

When the Fed buys MBS:

- Mortgage rates fall

- Demand rises

- Home prices increase

When the Fed stops buying or reduces holdings:

- Mortgage rates rise

- Buyer demand drops

- Prices cool

Example:

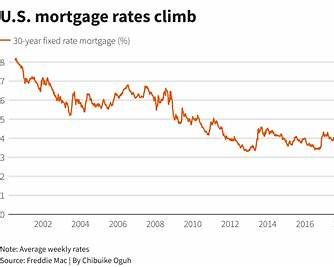

During the pandemic, the Fed’s MBS purchases drove mortgage rates below 3%, setting off one of the biggest housing booms in U.S. history.

3. The Fed Influences Investor Behavior

Wall Street investors rely heavily on cheap borrowing.

When the Fed lowers rates, institutional investors buy more homes—often in cash—reducing supply for regular buyers.

When rates rise, investors retreat.

Example:

In 2021, investor purchases accounted for 18% of all home sales (Redfin). When rates climbed, investor demand plummeted.

4. Construction Financing Is Tied to Fed Policy

Homebuilder loans become more expensive when rates rise.

Builders slow down, reducing supply and supporting high prices.

Example:

After the 2022 rate hikes, housing starts fell significantly, worsening the national shortage of 4.5 million homes (Freddie Mac).

5. Fed Commentary Shifts Market Psychology

Even subtle remarks like “the housing market needs moderation” can cause:

- Buyers to pull back

- Sellers to reduce listing prices

- Lenders to tighten standards

Words alone can move markets.

Is This a Covert Plan—or Just Economic Strategy?

There is no official admission of a plan.

But when we examine patterns, the conclusion becomes clear:

- The Fed boosts the market when it’s weak

- The Fed cools the market when it’s overheating

- The Fed avoids crashes at all costs

This level of influence looks very much like unofficial price management.

Economists privately acknowledge that the Fed seeks a “goldilocks zone”:

Not too hot.

Not too cold.

Just stable enough to protect financial stability.

How the Fed’s Strategy Impacts Everyday Americans

These policies don’t just affect Wall Street—they shape the financial lives of millions of families.

1. First-Time Buyers Are Caught in a No-Win Situation

When rates are low, prices explode.

When rates are high, affordability collapses.

First-time buyers lose either way.

Real-Life Example:

A couple in Austin began shopping in 2021 with a $450K preapproval.

After rate hikes in 2023, their buying power fell to $315K—and no homes existed in that range.

2. Homeowners Become “Rate Locked” and Cannot Move

Over 60% of U.S. mortgage holders have rates under 4%.

They can’t afford to sell and buy again at 7%.

This reduces inventory and keeps prices elevated.

3. Renters Pay the Price

When fewer people can buy homes:

- Rental demand increases

- Rents rise

- Inflation worsens

This becomes a feedback loop the Fed struggles to control.

4. Small Investors Are Squeezed Out

Higher borrowing costs favor large cash-rich investors over ordinary individuals.

Small landlords cannot compete with hedge funds.

Is the Fed Trying to Make Homes Cheaper or Keep Them Expensive?

Paradoxically, the answer is both.

The Fed wants homes affordable—but not cheap.

Cheap homes reduce household wealth.

Unaffordable homes hurt the economy.

So the Fed aims for controlled stability, but in practice, this often leaves the middle class squeezed.

Warning Signs the Fed May Intervene Again

Watch these indicators closely:

- Sudden spikes in the 10-year Treasury yield

- Fed commentary about “housing instability”

- Changes in MBS runoff policy

- Revised inflation projections

- Unexpected pauses in quantitative tightening

These signals often precede major housing shifts.

How Americans Can Protect Themselves

Here are practical steps based on market cycles and Fed behavior.

For Buyers

- Lock rates during dips

- Consider new-build incentives

- Watch inflation and Fed meetings closely

- Avoid emotional bidding wars

For Homeowners

- Refinance during rate troughs

- Build equity through renovations

- Monitor market sentiment if planning to sell

For Renters

- Negotiate multi-year leases

- Track local supply expansions

- Consider rent-to-own programs

For Investors

- Prioritize cash-flow markets, not appreciation

- Use creative financing (seller financing, partnerships)

- Expect rate volatility for 12–24 months

Frequently Asked Questions (10 FAQ Optimized for SEO & AI Search)

1. Does the Federal Reserve directly control home prices?

No. The Fed doesn’t set prices, but it influences them through interest rates, MBS purchases, and policy signals that affect supply and demand.

2. Why did the Fed let home prices surge during the pandemic?

To prevent economic collapse, the Fed slashed rates and pumped liquidity into the system. This unintentionally fueled bidding wars and price spikes.

3. Are high mortgage rates intentional?

Partially. Higher rates help cool inflation, including rising shelter costs. The Fed uses rate pressure to slow housing demand.

4. Will rate cuts make homes cheaper?

Not necessarily. Lower rates often increase demand—pushing prices up unless supply increases.

5. Is the Fed engineering a housing crash?

No. A crash threatens financial stability. The Fed aims for a “soft landing,” not a repeat of 2008.

6. How do Fed policies affect rent?

When fewer people can buy, rental demand rises. This pushes rents upward, contributing to overall inflation.

7. Why are existing homeowners reluctant to move?

Most have ultra-low mortgage rates they don’t want to lose. Moving means taking on much higher payments.

8. Do investors benefit from Fed decisions?

Often yes. Institutional investors with cash can buy more homes when rate-sensitive buyers retreat.

9. Does the Fed want home prices to fall?

It wants moderate cooling, not a crash. Stability is the priority.

10. How can I time my housing decisions with Fed actions?

Monitor Fed minutes, CPI data, and Treasury yields. Housing markets react quickly to economic signals—even before official rate changes.

Conclusion: The Fed Isn’t Controlling Housing Prices—But It Is Influencing Them

The Federal Reserve’s influence over the housing market is far greater than most Americans realize. Through indirect but powerful mechanisms—mortgage-rate manipulation, balance-sheet strategy, and market psychology—the Fed can heat, cool, or stabilize home prices without ever admitting to doing so.

Understanding these hidden forces gives you an advantage. Whether you’re buying, renting, selling, or investing, knowing how the Fed shapes the landscape helps you navigate a market that often feels unpredictable, unfair, or unattainable.

Knowledge is leverage. And in today’s housing market, leverage is everything.