Mortgage Rates Are About to Fall — Could This Trigger the Biggest Housing Boom Yet?

Mortgage rates are widely expected to decline as inflation cools and economic policy shifts. Even modest rate cuts could unlock massive pent-up demand from buyers sidelined for years. This in-depth analysis explores why rates may fall, whether a new housing boom could follow, and what buyers, sellers, and homeowners should do now to protect—or grow—their wealth.

Why Are Mortgage Rates Expected to Fall?

For the past few years, mortgage rates have dominated every housing conversation. After climbing rapidly to combat inflation, rates reshaped affordability and froze much of the housing market. But the underlying forces that pushed rates higher are beginning to ease.

Inflation, while still present, has cooled significantly from its peak. Supply chains have stabilized, consumer spending has slowed, and the Federal Reserve has signaled that aggressive rate hikes are no longer the default approach. While the Fed does not directly control mortgage rates, its guidance strongly influences bond markets, which ultimately determine long-term borrowing costs.

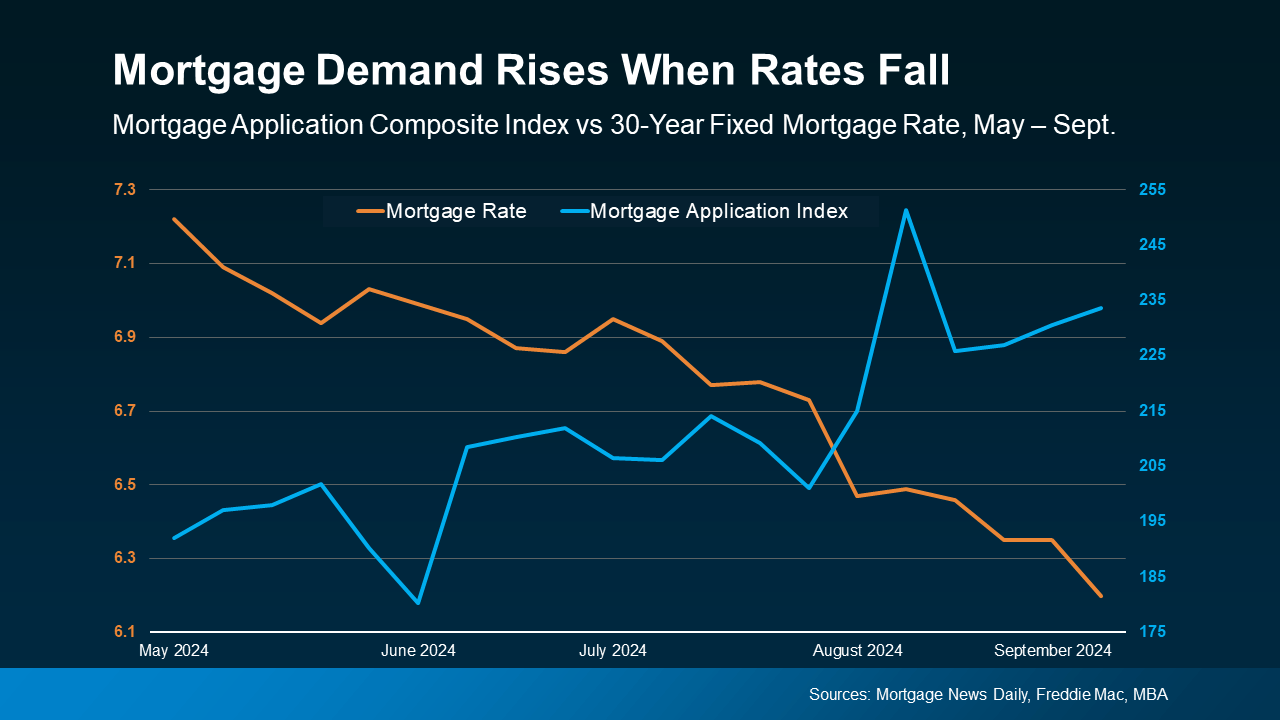

Historically, mortgage rates begin to fall before the Fed officially cuts rates. Markets move on expectations, not announcements. That’s why lenders and analysts are increasingly preparing for a downward shift—even if it happens gradually.

What Actually Determines Mortgage Rates?

Mortgage rates are influenced by several interconnected factors, not just one decision in Washington.

Key influences include:

- Inflation expectations

- Federal Reserve policy signals

- U.S. Treasury bond yields

- Global economic stability

When investors expect slower growth or lower inflation, they seek safer assets like bonds. As bond demand rises, yields fall—and mortgage rates typically follow.

This is why even rumors of economic cooling can push rates lower before official policy changes occur.

Why a Small Rate Drop Can Have a Huge Impact

Many Americans believe mortgage rates need to return to 3% to make a difference. That belief is misleading.

Even a modest drop can dramatically change affordability.

Real-life example:

Consider a $450,000 home with a 30-year fixed mortgage.

- At 7.5% interest: ≈ $3,147/month

- At 6.0% interest: ≈ $2,698/month

That’s more than $5,000 per year in savings—without changing the home price.

For households stretched by inflation, childcare costs, and everyday expenses, that difference can determine whether homeownership is possible.

The Massive Pent-Up Demand Beneath the Surface

One of the least discussed realities of today’s housing market is how many buyers are waiting.

These are not speculative investors chasing quick profits. They are:

- First-time buyers priced out by high monthly payments

- Families delaying moves for more space

- Renters watching affordability closely

According to the National Association of Realtors, millions of households postponed buying between 2022 and 2024, not because they lacked interest—but because affordability collapsed.

Lower rates could release that pressure quickly.

Could Falling Rates Trigger a Housing Boom?

The word “boom” evokes memories of reckless lending and runaway prices. But today’s environment is fundamentally different.

Why this wouldn’t mirror past bubbles:

- Lending standards remain strict

- Buyers are more financially cautious

- Investor speculation has cooled

Why demand could still surge:

- Housing supply remains historically low

- Household formation continues

- Rent remains expensive in many metros

Rather than a chaotic frenzy, a more likely scenario is a strong rebound in activity, especially in affordable and mid-priced markets.

The Lock-In Effect: Why Supply Is Still Tight

One major reason inventory remains low is the lock-in effect.

Millions of homeowners secured mortgages under 4%. Selling their home means giving up that rate and taking on a much higher one. This has discouraged listings, even among those who might otherwise move.

If mortgage rates fall meaningfully, that resistance weakens. More sellers may list—but demand could still outpace supply.

This imbalance is what gives falling rates their power.

What Falling Mortgage Rates Mean for Home Prices

Lower rates don’t automatically cause prices to skyrocket—but they do increase purchasing power.

When buyers can afford higher monthly payments:

- Competition increases

- Sellers regain leverage

- Prices stabilize or rise

In supply-constrained regions, even small demand increases can push prices upward.

This is why many analysts warn that waiting for rates to fall before buying can backfire.

Why the Next Housing Cycle Will Look Different

The last housing boom was driven by urgency and cheap money. The next cycle will likely be driven by readiness.

Buyers today are:

- More educated

- More payment-focused

- Less willing to overextend

That suggests a healthier market—but still a competitive one.

What This Means for Buyers Right Now

Buyers face a strategic choice: wait for lower rates or buy before competition returns.

Many experienced buyers choose a third option:

- Buy when the numbers make sense

- Refinance later if rates drop

This approach avoids bidding wars while preserving long-term flexibility.

What This Means for Sellers and Homeowners

For homeowners, falling rates can:

- Increase property values

- Improve refinancing opportunities

- Restore confidence in home equity

Sellers who prepare early—pricing correctly and improving presentation—may benefit most from renewed demand.

How Renters Are Affected

Lower mortgage rates don’t just help buyers.

As more renters transition into homeownership:

- Rental demand may ease

- Rent growth could slow

- Housing balance improves

This ripple effect supports broader affordability.

Risks That Could Prevent a Major Boom

No forecast is guaranteed.

Potential obstacles include:

- Economic slowdown or recession

- Job market weakness

- Unexpected inflation spikes

- Global instability

That’s why preparation matters more than prediction.

How to Position Your Wallet Before Rates Fall

Regardless of timing, proactive planning pays off.

Smart steps include:

- Improving credit scores

- Paying down high-interest debt

- Saving for down payments

- Monitoring local inventory

- Understanding refinancing options

Being financially ready is more powerful than guessing market turns.

Key Takeaways

- Mortgage rates are likely to trend lower

- Even small drops dramatically affect affordability

- Pent-up demand could re-enter quickly

- The next housing cycle will likely be disciplined, not reckless

- Preparation beats prediction

Frequently Asked Questions (FAQs)

1. Are mortgage rates really expected to fall soon?

Ans. Many economists expect gradual declines as inflation cools and monetary policy becomes less restrictive, though exact timing varies.

2. How much would rates need to fall to matter?

Ans. Even a 1% drop can significantly reduce monthly payments and improve affordability.

3. Could falling rates cause another housing bubble?

Ans. Unlikely. Lending standards and buyer behavior are far more conservative than during past bubbles.

4. Should I wait to buy until rates fall?

Ans. Waiting may increase competition. Many buyers prefer to buy when terms make sense and refinance later.

5. Will home prices rise if rates drop?

Ans. In supply-constrained markets, lower rates can increase demand and support higher prices.

6. Is refinancing worth it if rates decline?

Ans. Refinancing can be beneficial if the rate drop meaningfully reduces monthly payments.

7. How does the Federal Reserve influence mortgage rates?

Ans. The Fed affects rates indirectly through policy signals that move bond markets.

8. Will falling rates increase housing inventory?

Ans. Yes, lower rates can reduce the lock-in effect and encourage more sellers to list.

9. Which buyers benefit most from falling rates?

Ans. First-time buyers and payment-sensitive households often benefit the most.

10. How can I prepare financially for a housing rebound?

Ans. Improve credit, save cash, reduce debt, and study your local market carefully.

Final Thought

Mortgage rates don’t need to collapse to change the housing market.

They only need to fall enough to restore confidence.

When that happens, the next housing cycle won’t be driven by panic or speculation—but by preparation. Those who understand the signals early won’t just react to the next boom—they’ll be positioned for it.